How Exchange Fees Can Reduce Your Crypto Taxes In USA

Learn how exchange fees can lower your crypto tax bill in the USA this year 2024.

If you're a taxpayer in Norway who has invested in cryptocurrency, you might be wondering how to correctly share your crypto earnings on your tax form. Don't stress, you're not the only one! A lot of folks are a bit unsure about dealing with their crypto taxes, but with a bit of know-how and some guidance, it can be pretty easy to tackle.

To address this, we've compiled a thorough crypto tax guide specifically tailored for residents of Norway. Our goal is to untangle the complexities of crypto taxation, making it more approachable for everyone. This Detail guide covers everything you need to know about crypto taxation in Norway for the year 2024, and rest assured, we'll keep it regularly updated to reflect any new regulations issued by Skatteetaten, the Norwegian Tax Authority.

So, let's get started…

The Norwegian Tax Administration, known as Skatteetaten, categorizes cryptocurrencies as virtual currencies falling under the broader tax regulations for assets. Despite some similarities to fiat money, such as the Norwegian Kroner, virtual currencies are not considered ordinary currencies due to the lack of issuance or guarantee by a national central bank.

Key Takeaway: Whether you've bought, sold, mined, or hold virtual currency assets like Ethereum (ETH) or Bitcoin (BTC), reporting these activities in your tax return is a must.

Norwegian taxpayers need to navigate through two types of taxes concerning their crypto holdings:

Wealth tax encompasses cryptocurrencies, requiring individuals and businesses to pay municipal and state taxes on their net wealth. Calculating net wealth involves subtracting deductible debt from the total market value of assets, including crypto holdings, on January 1st of each year.

Have you ever considered that whenever you sell, trade, or use Bitcoin or other cryptocurrencies to buy goods or services, you might need to report it as a capital Income on your taxes? Many people mistakenly believe that taxes only apply when converting crypto to fiat currency like NOK. However, that's not the case. In fact, a variety of transactions fall under taxable events, including:

It's crucial to report and pay capital income tax for your cryptocurrency transactions to stay in line with the law. Failing to do so may lead to penalties and fines.

The process of calculating your capital income can be complex. You need to assess how much your cryptocurrency has gained in value since you obtained it. The total cost of acquiring the cryptocurrency, which includes any fees paid, is referred to as the acquisition cost.

If you've acquired cryptocurrency through multiple transactions, pinpointing the specific units you're selling can be challenging, impacting your profits. In Norway, there are various methods available to determine which cryptocurrency units you're selling, such as the FIFO (First-In-First-Out), LIFO (Last-In-First-Out), and HIFO (Highest-In-First-Out) methods.

In Norway, capital income is subject to a flat 22% tax rate. The general income tax rate is 22%, but residents of Finnmark and Nord-Troms enjoy a reduced rate of 18.5%. The step tax, operating on four levels, imposes a 1.7% tax on income between 198,350 NOK and 279,149 NOK, a 4% tax on income from 279,150 NOK to 642,949 NOK, and a 13.5% (or 11.5% for specific regions) tax on income from 642,950 NOK to 926,799 NOK. Incomes between 926,800 NOK and 1,499,999 NOK face a 16.5% step tax, and earnings over 1.5 million kroner are taxed at a 17.5% rate.

Key Deadline: The tax year in Norway runs from January 1st to December 31st, with a filing deadline on April 30th. Extensions may be granted in special cases.

Contrary to popular belief that cryptocurrency transactions are anonymous, Skatteetaten has robust mechanisms to track crypto ownership and trades. Cryptocurrency exchanges and digital asset investments are subject to Know-Your-Customer (KYC) identification applications, making it easier for Skatteetaten to obtain information. Additionally, due to the country's inclusion in the European Economic Area (EEA), data sharing agreements with the EU can further enhance Skatteetaten's access to relevant information.

Important Note: Skatteetaten can request documents during audits, including bank statements, transaction overviews, and reports from crypto-related platforms. Non-compliance may result in harsh penalties.

Understanding how to calculate and report crypto taxes is crucial for Norwegian investors. Skatteetaten requires individuals to declare their cryptocurrency wealth, capital income. Here's a closer look at the key components of the process:

Step 1: Calculate Cost Basis

To streamline your crypto tax reporting, start by calculating the cost basis for each asset you've swapped, sold, or gifted in a tax year. This involves adding the acquisition cost and any associated fees (like transaction or gas fees).

Step 2: Compute Capital Income

Once the cost basis is established, calculating your capital income is straightforward. Subtract the cost basis from the disposal amount. If the result is positive, indicating an Income, it's subject to a flat income tax rate of 22%. If negative, it represents a loss. Although no tax liabilities arise from losses, tracking and reporting them to the relevant tax authorities, such as Skatteetaten, is crucial for effectively reducing your overall tax bill.

Example Transactions:

03/02/2023: David buys 0.5 BTC for 80,000 NOK

06/04/2023: David buys 3 ETH for 15,000 NOK each

05/06/2023: David buys 1 BTC for 1,70,000 NOK and 2 ETH for 16,000 NOK each

13/06/2023: David sells 1 BTC for 1,80,000 NOK

19/08/2024: David sells 3 ETH for 19,000 NOK each

1st Disposal

In this transaction, David decides to sell 1 BTC for 180,000 NOK. To calculate the income, we're using the FIFO accounting method, as recommended by Skatteetaten. This method, known as First-In-First-Out, essentially means that the first asset you purchase is the first one you sell.

Now, let's break down the specifics of this sale involving sale of 1 BTC:

BTC Cost base:

Total Income on Sale of 1 BTC: 180,000 - 165,000 = 15,000 NOK

2nd Disposal

Transaction History:

Capital Income Calculation:

The capital Income on the sale of 1 ETH is 12,000 NOK.

In Norway, when it comes to calculating the cost basis for your crypto assets, the go-to method is FIFO, which stands for First-In, First-Out (Please refer to the above Crypto income calculations example for FIFO method). Simply put, this means that when you decide to sell any of your crypto or other assets, the cost basis is determined by the price and date of the oldest asset you own.

It's worth noting that FIFO is the default method in Norway, but there are alternative methods like LIFO (Last-In, First-Out) and HIFO. However, these alternatives need specific approval from tax authorities and are typically limited to certain businesses or taxpayers.

Here's a quick overview of the other accounting methods:

While FIFO is the standard, exploring these alternatives may be relevant for specific businesses or taxpayers with approval from tax authorities.

In Norway, the taxation of cryptocurrencies extends beyond transactions and Income; it encompasses an often-overlooked aspect known as Wealth Tax. This tax is applied to the total net wealth of individuals, including their cryptocurrency holdings. To navigate this facet of taxation effectively, it's crucial to comprehend the key elements and calculations involved.

Example:

12/02/2023: Lucy buys 1 BTC for 180,000 NOK

15/04/2023: Lucy buys 10 ETH for 14,000 NOK each

02/05/2024: Lucy sells 1 BTC for 200,000 NOK

05/06/2024: Lucy sells 5 ETH for 18,000 NOK each

Assuming Lucy initially had assets worth 1,800,000 NOK in her portfolio and a 300,000 NOK debt before these transactions, let's explore the Capital Income and wealth tax implications.

Calculating Capital Income:

1st Disposal (1 BTC):

2nd Disposal (5 ETH):

Collective Income for both disposals: 20,000 + 20,000 = 40,000 NOK

This total represents the amount subject to income tax.

Calculating Net Wealth:

Considering Lucy didn't make other transactions throughout the year, except those mentioned above, and she still holds 5 ETH:

Since Lucy's net wealth is less than 1,700,000 NOK, she is not obligated to pay any wealth tax.

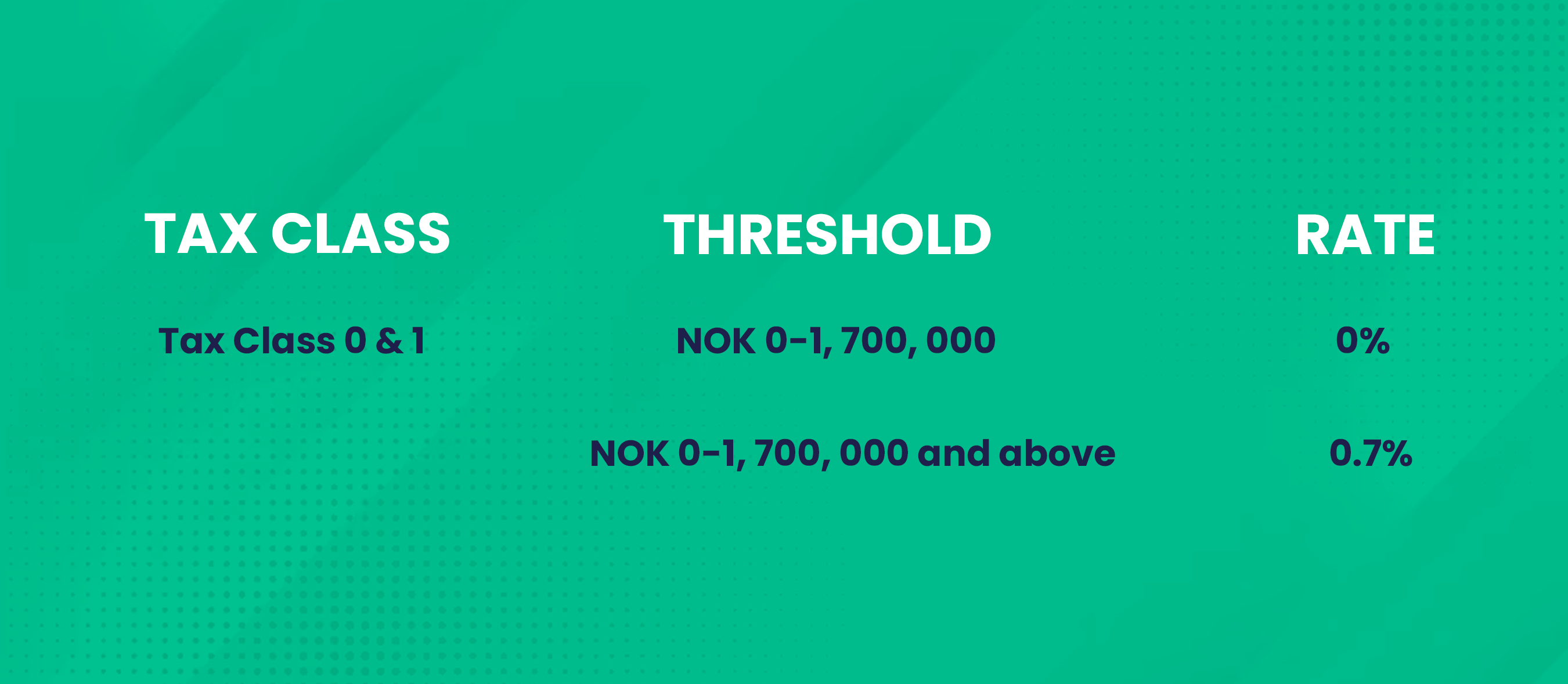

Wealth Tax is further categorized into tax classes, each with its own threshold and rate. Understanding your tax class is crucial, as it directly influences the amount of Wealth Tax you may be required to pay.

Decentralized finance (DeFi) introduces unique challenges and considerations for cryptocurrency taxation in Norway. Skatteetaten, the Norwegian Tax Authority, has outlined specific guidelines regarding DeFi transactions, emphasizing the need for income tax payments and meticulous record-keeping.

Skatteetaten categorizes various DeFi transactions as taxable events. It's imperative for individuals engaged in DeFi activities to assess and report any profits, losses, or income generated from these transactions. Key taxable DeFi events, as defined by Skatteetaten, include:

1. Swap/Exchange of Cryptocurrency and Token:

The act of swapping or exchanging one cryptocurrency or token for another is considered a realization event, triggering tax obligations.

2. Exchange to and from Wrapped Token:

Transactions involving the exchange to and from wrapped tokens are also considered realization events, attracting income tax liabilities.

3. Deposits in Liquidity Pools:

Depositing assets into liquidity pools in exchange for a liquidity pool token or its equivalent is deemed a realization event, subject to taxation.

4. Returns from Liquidity Pools:

Profits derived from participating in liquidity pools are considered taxable income. Whether the return results from a change in underlying value or is triggered by realization, it is subject to taxation.

5. Receipt of Management Token:

The receipt of a management token is treated as income upon receipt. Subsequent sale or exchange of the token falls under realization, contributing to capital income sections of the tax guide.

In Norway, Non-Fungible Tokens (NFTs) are recognized as assets by Skatteetaten, and they are subject to the same tax rules as other virtual assets. While NFTs can serve various purposes, including digital art, collectibles, and in-game items, the tax treatment remains consistent.

1. Minting NFTs

The act of creating or minting an NFT can have tax implications. Minting becomes taxable if the smart contract involved in the process includes the disposal of an asset, such as Ethereum (ETH). However, if minting does not involve the disposal of assets, as is the case with some free mints, it does not trigger taxation.

2. NFT Sales

Selling an NFT is treated as a realization event, and capital Income are calculated using the formula:

Capital Income = Capital Proceeds of NFT Sale − (Transaction Costs + Cost Basis)

3. Income and Royalties

Any income or royalties derived from the initial sale or subsequent sales of NFTs are taxable in Norway. It's important to keep correct records of these transactions for proper reporting.

Understanding the tax treatment of NFTs is essential for individuals engaged in activities such as digital art creation, NFT trading, and participation in NFT marketplaces.

Not all crypto transactions attract taxes in Norway. Certain events are considered non-taxable, providing an opportunity for investors to optimize their tax position. Here are some non-taxable crypto transactions:

1. Lost or Stolen Crypto

Norway allows deductions for lost crypto due to scams, provided the investor has made efforts to recover the lost funds. Caution is advised when dealing with smart contracts and potential scams.

2. Transfers Between Wallets

Transferring crypto between personal wallets and exchanges is not a taxable event. Only the transfer fee incurs tax, offering flexibility for investors to manage their holdings.

3. Gift Transactions

Norway does not impose gift taxes. However, it's essential to maintain records of the gift's origin and cost basis for documentation purposes.

While all crypto is taxable and reported annually, specific crypto assets may generate interest or rewards. Examples of such assets, along with potential tax deductions, include:

1. Sale of Crypto Assets: Profit from selling cryptocurrencies is subject to capital income tax, with rates at 22% for individuals and 25% for companies.

2. Mining: becomes taxable when cryptocurrency is received, and records of the market value at the time of receipt are crucial. Deductions can be claimed for equipment, software, and electricity with a 30% annual depreciation.

Here what Skatteetaten says about mining

“Mining of virtual currency means that you receive virtual currency in return for verification activity. Mining usually requires computing power for the method ‘Proof of Work’ to verify transactions on the blockchain and to extract virtual currency.”

3. Staking: Proof of Stake (PoS) staking is treated similarly to mining income, with deductions available for associated expenses.

4. Referral Rewards: Income from affiliate programs in cryptocurrency, such as referral rewards, is taxable and must be reported.

5. Returns from Liquidity Pools: Returns from participating in liquidity pools are considered taxable income, independent of whether the return comes as a change in underlying value or as a token providing income upon receipt.

Certain crypto transactions fall into grey areas, where specific regulations are not explicitly outlined or are considered on a case-by-case basis. These include:

1. Forks

Forks are considered income at market value when received, and the tax treatment can vary. Given the historical volatility of forks, seeking advice from a specialist is recommended.

2. Initial Coin Offerings (ICOs)

ICOs are assessed on a case-by-case basis to determine tax and value-added tax (VAT) liability. Consulting with an accountant is advisable for individuals participating in ICOs.

3. Cryptocurrency Donations

Donating cryptocurrency may be tax-deductible, but it's essential to discuss this with an accountant to ensure the foundation receives state aid in the year of the gift. Additionally, confirmation that the virtual currency falls within the range of "amount between NOK 500 and 30,000" is essential.

4. Airdrops

While airdrops potentially fall under gifts in Norway, there is no explicit mention of them by Skatteetaten. Consulting with an accountant is recommended, and by default, airdrops are considered income.

5. Lending and Borrowing Crypto

Lending and borrowing crypto could potentially be viewed as disposal events in Norway. Individuals involved in these activities should discuss the circumstances with a tax professional.

Navigating these grey areas requires careful consideration and expert advice. CryptoTaxCalculator recommends discussing specific situations with a tax professional for clear guidance.

If you're a crypto trader or investor in Norway, understanding how to report your crypto taxes is crucial. Luckily, Skatteetaten has streamlined this process, making it user-friendly through its online tax portal.

Submitting your taxes has never been more accessible – you can choose to do it online or via mail, aligning with your preferences. The submission encompasses wealth, capital income tax, ensuring a comprehensive approach to your financial obligations.

Questions or need guidance?

Skatteetaten is just a call away, available for assistance between 9:00 and 15:00 on weekdays. And for those outside Norway, reaching out is equally straightforward. Dial +47 22 07 70 00 or 800 80 000, and the Norwegian tax authority is ready to guide you through the intricacies of crypto taxation.

New to the tax-filing process or want a visual guide? Skatteetaten goes the extra mile by offering a video guide on filing your crypto taxes, a handy resource for first-time filers.

Our guide here focuses on the online filing method provided by Skatteetaten. If you opt for their online platform, follow these steps to ensure a smooth process and steer clear of potential tax complications in the future.

Before the filing process, ensure you have all the necessary documentation at hand. Skatteetaten may request these documents to substantiate the positions taken on your tax returns. Key documents include:

Option 1: Individual Cryptocurrency Entries for Seamless Reporting

Option 2: Streamlined Entries for Multiple Virtual Currencies

After inputting data with either option, scroll down to "Årsak til endring/nye opplysninger" (reason for the change/new information), tick the box "Lagt til opplysninger som manglet" (Added information that was missing), and click "Ok". This ensures your successful crypto tax return submission to Skattetaten.

Although this process may appear intricate, worry not. Platforms like Kryptos offer an online solution, guiding you through each step, identifying potential deductions and credits, and facilitating quick e-filing of your tax return with Skatteetaten. Simplify your crypto tax journey with Kryptos today!

For a streamlined tax filing experience, platforms like Kryptos can simplify the process. Here's a step-wise breakdown:

1. Sign Up on Kryptos: Visit Kryptos and sign up using your email or Google/Apple account.

2. Set Up Your Account: Choose your country, currency, time zone, and taxation method.

3. Add Your Wallets and Exchanges: Connect your wallets and exchanges to Kryptos for automatic data import.

4. Review and Classify Transactions: Kryptos automatically categorizes your transactions. Review and make adjustments as needed.

5. Generate Tax Reports: Kryptos provides detailed tax reports, including capital income and wealth reports.

6. Export and File: Export the generated reports and follow Skatteetaten's guidelines to file your crypto taxes.

If you find yourself needing more clarity on integrating or creating your tax reports, feel free to check out our video guide available here.

While completely dodging crypto taxes is not an option, the Norwegian tax authorities provide some legitimate ways to ease your tax stress:

Absolutely, cryptocurrency is entirely legal in Norway. Recognized by the government as an asset and a valid form of payment, cryptocurrency exchanges in Norway are regulated by the Financial Supervisory Authority (FSA). Since 2019, regulations mandate exchanges to register with the FSA, ensuring compliance with anti-money laundering (AML) and counter-terrorist financing (CTF) measures. Furthermore, both individuals and businesses face no restrictions on holding or engaging in cryptocurrency mining.

Cryptocurrency transactions in Norway are subject to taxation, falling under two categories: Capital income tax and wealth tax. income generated from crypto transactions are taxed according to income tax laws, and crypto assets are considered in net wealth calculations, attracting a marginal wealth tax. Refer to the detailed tax guide above for comprehensive information on crypto taxation in Norway.

No, the act of buying crypto with fiat currency is not a taxable event in itself. However, it becomes taxable if it involves the disposal of another asset. Essentially, purchasing crypto with fiat currency is non-taxable, but if you use one crypto asset to pay for another, it constitutes a taxable event.

Simplify your crypto tax filing process using Kryptos, a user-friendly crypto tax software. By logging into the platform and adding your trading accounts, wallets, and DeFi accounts, Kryptos automates the entire process. Let Kryptos do the heavy lifting – it can auto-fetch all your transactions from the tax year, generate a legally compliant tax report within minutes, and even suggest strategies to minimize your tax liability. Experience the magic of hassle-free crypto tax filing with Kryptos. Give it a try today!

All content on Kryptos serves general informational purposes only. It's not intended to replace any professional advice from licensed accountants, attorneys, or certified financial and tax professionals. The information is completed to the best of our knowledge and we at Kryptos do not claim either correctness or accuracy of the same. Before taking any tax position / stance, you should always consider seeking independent legal, financial, taxation or other advice from the professionals. Kryptos is not liable for any loss caused from the use of, or by placing reliance on, the information on this website. Kryptos disclaims any responsibility for the accuracy or adequacy of any positions taken by you in your tax returns. Thank you for being part of our community, and we're excited to continue guiding you on your crypto journey!

Learn how exchange fees can lower your crypto tax bill in the USA this year 2024.

Are you ready to File your Crypto taxes? Then make sure you do it right. Learn what crypto tax forms you'll need and how to report your crypto activities to the IRS before April 15th.

Earning income through crypto mining? This guide will help you understand how your mining rewards are taxed in the USA.

If you're a taxpayer in Norway who has invested in cryptocurrency, you might be wondering how to correctly share your crypto earnings on your tax form. Don't stress, you're not the only one! A lot of folks are a bit unsure about dealing with their crypto taxes, but with a bit of know-how and some guidance, it can be pretty easy to tackle.

To address this, we've compiled a thorough crypto tax guide specifically tailored for residents of Norway. Our goal is to untangle the complexities of crypto taxation, making it more approachable for everyone. This Detail guide covers everything you need to know about crypto taxation in Norway for the year 2024, and rest assured, we'll keep it regularly updated to reflect any new regulations issued by Skatteetaten, the Norwegian Tax Authority.

So, let's get started…

The Norwegian Tax Administration, known as Skatteetaten, categorizes cryptocurrencies as virtual currencies falling under the broader tax regulations for assets. Despite some similarities to fiat money, such as the Norwegian Kroner, virtual currencies are not considered ordinary currencies due to the lack of issuance or guarantee by a national central bank.

Key Takeaway: Whether you've bought, sold, mined, or hold virtual currency assets like Ethereum (ETH) or Bitcoin (BTC), reporting these activities in your tax return is a must.

Norwegian taxpayers need to navigate through two types of taxes concerning their crypto holdings:

Wealth tax encompasses cryptocurrencies, requiring individuals and businesses to pay municipal and state taxes on their net wealth. Calculating net wealth involves subtracting deductible debt from the total market value of assets, including crypto holdings, on January 1st of each year.

Have you ever considered that whenever you sell, trade, or use Bitcoin or other cryptocurrencies to buy goods or services, you might need to report it as a capital Income on your taxes? Many people mistakenly believe that taxes only apply when converting crypto to fiat currency like NOK. However, that's not the case. In fact, a variety of transactions fall under taxable events, including:

It's crucial to report and pay capital income tax for your cryptocurrency transactions to stay in line with the law. Failing to do so may lead to penalties and fines.

The process of calculating your capital income can be complex. You need to assess how much your cryptocurrency has gained in value since you obtained it. The total cost of acquiring the cryptocurrency, which includes any fees paid, is referred to as the acquisition cost.

If you've acquired cryptocurrency through multiple transactions, pinpointing the specific units you're selling can be challenging, impacting your profits. In Norway, there are various methods available to determine which cryptocurrency units you're selling, such as the FIFO (First-In-First-Out), LIFO (Last-In-First-Out), and HIFO (Highest-In-First-Out) methods.

In Norway, capital income is subject to a flat 22% tax rate. The general income tax rate is 22%, but residents of Finnmark and Nord-Troms enjoy a reduced rate of 18.5%. The step tax, operating on four levels, imposes a 1.7% tax on income between 198,350 NOK and 279,149 NOK, a 4% tax on income from 279,150 NOK to 642,949 NOK, and a 13.5% (or 11.5% for specific regions) tax on income from 642,950 NOK to 926,799 NOK. Incomes between 926,800 NOK and 1,499,999 NOK face a 16.5% step tax, and earnings over 1.5 million kroner are taxed at a 17.5% rate.

Key Deadline: The tax year in Norway runs from January 1st to December 31st, with a filing deadline on April 30th. Extensions may be granted in special cases.

Contrary to popular belief that cryptocurrency transactions are anonymous, Skatteetaten has robust mechanisms to track crypto ownership and trades. Cryptocurrency exchanges and digital asset investments are subject to Know-Your-Customer (KYC) identification applications, making it easier for Skatteetaten to obtain information. Additionally, due to the country's inclusion in the European Economic Area (EEA), data sharing agreements with the EU can further enhance Skatteetaten's access to relevant information.

Important Note: Skatteetaten can request documents during audits, including bank statements, transaction overviews, and reports from crypto-related platforms. Non-compliance may result in harsh penalties.

Understanding how to calculate and report crypto taxes is crucial for Norwegian investors. Skatteetaten requires individuals to declare their cryptocurrency wealth, capital income. Here's a closer look at the key components of the process:

Step 1: Calculate Cost Basis

To streamline your crypto tax reporting, start by calculating the cost basis for each asset you've swapped, sold, or gifted in a tax year. This involves adding the acquisition cost and any associated fees (like transaction or gas fees).

Step 2: Compute Capital Income

Once the cost basis is established, calculating your capital income is straightforward. Subtract the cost basis from the disposal amount. If the result is positive, indicating an Income, it's subject to a flat income tax rate of 22%. If negative, it represents a loss. Although no tax liabilities arise from losses, tracking and reporting them to the relevant tax authorities, such as Skatteetaten, is crucial for effectively reducing your overall tax bill.

Example Transactions:

03/02/2023: David buys 0.5 BTC for 80,000 NOK

06/04/2023: David buys 3 ETH for 15,000 NOK each

05/06/2023: David buys 1 BTC for 1,70,000 NOK and 2 ETH for 16,000 NOK each

13/06/2023: David sells 1 BTC for 1,80,000 NOK

19/08/2024: David sells 3 ETH for 19,000 NOK each

1st Disposal

In this transaction, David decides to sell 1 BTC for 180,000 NOK. To calculate the income, we're using the FIFO accounting method, as recommended by Skatteetaten. This method, known as First-In-First-Out, essentially means that the first asset you purchase is the first one you sell.

Now, let's break down the specifics of this sale involving sale of 1 BTC:

BTC Cost base:

Total Income on Sale of 1 BTC: 180,000 - 165,000 = 15,000 NOK

2nd Disposal

Transaction History:

Capital Income Calculation:

The capital Income on the sale of 1 ETH is 12,000 NOK.

In Norway, when it comes to calculating the cost basis for your crypto assets, the go-to method is FIFO, which stands for First-In, First-Out (Please refer to the above Crypto income calculations example for FIFO method). Simply put, this means that when you decide to sell any of your crypto or other assets, the cost basis is determined by the price and date of the oldest asset you own.

It's worth noting that FIFO is the default method in Norway, but there are alternative methods like LIFO (Last-In, First-Out) and HIFO. However, these alternatives need specific approval from tax authorities and are typically limited to certain businesses or taxpayers.

Here's a quick overview of the other accounting methods:

While FIFO is the standard, exploring these alternatives may be relevant for specific businesses or taxpayers with approval from tax authorities.

In Norway, the taxation of cryptocurrencies extends beyond transactions and Income; it encompasses an often-overlooked aspect known as Wealth Tax. This tax is applied to the total net wealth of individuals, including their cryptocurrency holdings. To navigate this facet of taxation effectively, it's crucial to comprehend the key elements and calculations involved.

Example:

12/02/2023: Lucy buys 1 BTC for 180,000 NOK

15/04/2023: Lucy buys 10 ETH for 14,000 NOK each

02/05/2024: Lucy sells 1 BTC for 200,000 NOK

05/06/2024: Lucy sells 5 ETH for 18,000 NOK each

Assuming Lucy initially had assets worth 1,800,000 NOK in her portfolio and a 300,000 NOK debt before these transactions, let's explore the Capital Income and wealth tax implications.

Calculating Capital Income:

1st Disposal (1 BTC):

2nd Disposal (5 ETH):

Collective Income for both disposals: 20,000 + 20,000 = 40,000 NOK

This total represents the amount subject to income tax.

Calculating Net Wealth:

Considering Lucy didn't make other transactions throughout the year, except those mentioned above, and she still holds 5 ETH:

Since Lucy's net wealth is less than 1,700,000 NOK, she is not obligated to pay any wealth tax.

Wealth Tax is further categorized into tax classes, each with its own threshold and rate. Understanding your tax class is crucial, as it directly influences the amount of Wealth Tax you may be required to pay.

Decentralized finance (DeFi) introduces unique challenges and considerations for cryptocurrency taxation in Norway. Skatteetaten, the Norwegian Tax Authority, has outlined specific guidelines regarding DeFi transactions, emphasizing the need for income tax payments and meticulous record-keeping.

Skatteetaten categorizes various DeFi transactions as taxable events. It's imperative for individuals engaged in DeFi activities to assess and report any profits, losses, or income generated from these transactions. Key taxable DeFi events, as defined by Skatteetaten, include:

1. Swap/Exchange of Cryptocurrency and Token:

The act of swapping or exchanging one cryptocurrency or token for another is considered a realization event, triggering tax obligations.

2. Exchange to and from Wrapped Token:

Transactions involving the exchange to and from wrapped tokens are also considered realization events, attracting income tax liabilities.

3. Deposits in Liquidity Pools:

Depositing assets into liquidity pools in exchange for a liquidity pool token or its equivalent is deemed a realization event, subject to taxation.

4. Returns from Liquidity Pools:

Profits derived from participating in liquidity pools are considered taxable income. Whether the return results from a change in underlying value or is triggered by realization, it is subject to taxation.

5. Receipt of Management Token:

The receipt of a management token is treated as income upon receipt. Subsequent sale or exchange of the token falls under realization, contributing to capital income sections of the tax guide.

In Norway, Non-Fungible Tokens (NFTs) are recognized as assets by Skatteetaten, and they are subject to the same tax rules as other virtual assets. While NFTs can serve various purposes, including digital art, collectibles, and in-game items, the tax treatment remains consistent.

1. Minting NFTs

The act of creating or minting an NFT can have tax implications. Minting becomes taxable if the smart contract involved in the process includes the disposal of an asset, such as Ethereum (ETH). However, if minting does not involve the disposal of assets, as is the case with some free mints, it does not trigger taxation.

2. NFT Sales

Selling an NFT is treated as a realization event, and capital Income are calculated using the formula:

Capital Income = Capital Proceeds of NFT Sale − (Transaction Costs + Cost Basis)

3. Income and Royalties

Any income or royalties derived from the initial sale or subsequent sales of NFTs are taxable in Norway. It's important to keep correct records of these transactions for proper reporting.

Understanding the tax treatment of NFTs is essential for individuals engaged in activities such as digital art creation, NFT trading, and participation in NFT marketplaces.

Not all crypto transactions attract taxes in Norway. Certain events are considered non-taxable, providing an opportunity for investors to optimize their tax position. Here are some non-taxable crypto transactions:

1. Lost or Stolen Crypto

Norway allows deductions for lost crypto due to scams, provided the investor has made efforts to recover the lost funds. Caution is advised when dealing with smart contracts and potential scams.

2. Transfers Between Wallets

Transferring crypto between personal wallets and exchanges is not a taxable event. Only the transfer fee incurs tax, offering flexibility for investors to manage their holdings.

3. Gift Transactions

Norway does not impose gift taxes. However, it's essential to maintain records of the gift's origin and cost basis for documentation purposes.

While all crypto is taxable and reported annually, specific crypto assets may generate interest or rewards. Examples of such assets, along with potential tax deductions, include:

1. Sale of Crypto Assets: Profit from selling cryptocurrencies is subject to capital income tax, with rates at 22% for individuals and 25% for companies.

2. Mining: becomes taxable when cryptocurrency is received, and records of the market value at the time of receipt are crucial. Deductions can be claimed for equipment, software, and electricity with a 30% annual depreciation.

Here what Skatteetaten says about mining

“Mining of virtual currency means that you receive virtual currency in return for verification activity. Mining usually requires computing power for the method ‘Proof of Work’ to verify transactions on the blockchain and to extract virtual currency.”

3. Staking: Proof of Stake (PoS) staking is treated similarly to mining income, with deductions available for associated expenses.

4. Referral Rewards: Income from affiliate programs in cryptocurrency, such as referral rewards, is taxable and must be reported.

5. Returns from Liquidity Pools: Returns from participating in liquidity pools are considered taxable income, independent of whether the return comes as a change in underlying value or as a token providing income upon receipt.

Certain crypto transactions fall into grey areas, where specific regulations are not explicitly outlined or are considered on a case-by-case basis. These include:

1. Forks

Forks are considered income at market value when received, and the tax treatment can vary. Given the historical volatility of forks, seeking advice from a specialist is recommended.

2. Initial Coin Offerings (ICOs)

ICOs are assessed on a case-by-case basis to determine tax and value-added tax (VAT) liability. Consulting with an accountant is advisable for individuals participating in ICOs.

3. Cryptocurrency Donations

Donating cryptocurrency may be tax-deductible, but it's essential to discuss this with an accountant to ensure the foundation receives state aid in the year of the gift. Additionally, confirmation that the virtual currency falls within the range of "amount between NOK 500 and 30,000" is essential.

4. Airdrops

While airdrops potentially fall under gifts in Norway, there is no explicit mention of them by Skatteetaten. Consulting with an accountant is recommended, and by default, airdrops are considered income.

5. Lending and Borrowing Crypto

Lending and borrowing crypto could potentially be viewed as disposal events in Norway. Individuals involved in these activities should discuss the circumstances with a tax professional.

Navigating these grey areas requires careful consideration and expert advice. CryptoTaxCalculator recommends discussing specific situations with a tax professional for clear guidance.

If you're a crypto trader or investor in Norway, understanding how to report your crypto taxes is crucial. Luckily, Skatteetaten has streamlined this process, making it user-friendly through its online tax portal.

Submitting your taxes has never been more accessible – you can choose to do it online or via mail, aligning with your preferences. The submission encompasses wealth, capital income tax, ensuring a comprehensive approach to your financial obligations.

Questions or need guidance?

Skatteetaten is just a call away, available for assistance between 9:00 and 15:00 on weekdays. And for those outside Norway, reaching out is equally straightforward. Dial +47 22 07 70 00 or 800 80 000, and the Norwegian tax authority is ready to guide you through the intricacies of crypto taxation.

New to the tax-filing process or want a visual guide? Skatteetaten goes the extra mile by offering a video guide on filing your crypto taxes, a handy resource for first-time filers.

Our guide here focuses on the online filing method provided by Skatteetaten. If you opt for their online platform, follow these steps to ensure a smooth process and steer clear of potential tax complications in the future.

Before the filing process, ensure you have all the necessary documentation at hand. Skatteetaten may request these documents to substantiate the positions taken on your tax returns. Key documents include:

Option 1: Individual Cryptocurrency Entries for Seamless Reporting

Option 2: Streamlined Entries for Multiple Virtual Currencies

After inputting data with either option, scroll down to "Årsak til endring/nye opplysninger" (reason for the change/new information), tick the box "Lagt til opplysninger som manglet" (Added information that was missing), and click "Ok". This ensures your successful crypto tax return submission to Skattetaten.

Although this process may appear intricate, worry not. Platforms like Kryptos offer an online solution, guiding you through each step, identifying potential deductions and credits, and facilitating quick e-filing of your tax return with Skatteetaten. Simplify your crypto tax journey with Kryptos today!

For a streamlined tax filing experience, platforms like Kryptos can simplify the process. Here's a step-wise breakdown:

1. Sign Up on Kryptos: Visit Kryptos and sign up using your email or Google/Apple account.

2. Set Up Your Account: Choose your country, currency, time zone, and taxation method.

3. Add Your Wallets and Exchanges: Connect your wallets and exchanges to Kryptos for automatic data import.

4. Review and Classify Transactions: Kryptos automatically categorizes your transactions. Review and make adjustments as needed.

5. Generate Tax Reports: Kryptos provides detailed tax reports, including capital income and wealth reports.

6. Export and File: Export the generated reports and follow Skatteetaten's guidelines to file your crypto taxes.

If you find yourself needing more clarity on integrating or creating your tax reports, feel free to check out our video guide available here.

While completely dodging crypto taxes is not an option, the Norwegian tax authorities provide some legitimate ways to ease your tax stress:

Absolutely, cryptocurrency is entirely legal in Norway. Recognized by the government as an asset and a valid form of payment, cryptocurrency exchanges in Norway are regulated by the Financial Supervisory Authority (FSA). Since 2019, regulations mandate exchanges to register with the FSA, ensuring compliance with anti-money laundering (AML) and counter-terrorist financing (CTF) measures. Furthermore, both individuals and businesses face no restrictions on holding or engaging in cryptocurrency mining.

Cryptocurrency transactions in Norway are subject to taxation, falling under two categories: Capital income tax and wealth tax. income generated from crypto transactions are taxed according to income tax laws, and crypto assets are considered in net wealth calculations, attracting a marginal wealth tax. Refer to the detailed tax guide above for comprehensive information on crypto taxation in Norway.

No, the act of buying crypto with fiat currency is not a taxable event in itself. However, it becomes taxable if it involves the disposal of another asset. Essentially, purchasing crypto with fiat currency is non-taxable, but if you use one crypto asset to pay for another, it constitutes a taxable event.

Simplify your crypto tax filing process using Kryptos, a user-friendly crypto tax software. By logging into the platform and adding your trading accounts, wallets, and DeFi accounts, Kryptos automates the entire process. Let Kryptos do the heavy lifting – it can auto-fetch all your transactions from the tax year, generate a legally compliant tax report within minutes, and even suggest strategies to minimize your tax liability. Experience the magic of hassle-free crypto tax filing with Kryptos. Give it a try today!

All content on Kryptos serves general informational purposes only. It's not intended to replace any professional advice from licensed accountants, attorneys, or certified financial and tax professionals. The information is completed to the best of our knowledge and we at Kryptos do not claim either correctness or accuracy of the same. Before taking any tax position / stance, you should always consider seeking independent legal, financial, taxation or other advice from the professionals. Kryptos is not liable for any loss caused from the use of, or by placing reliance on, the information on this website. Kryptos disclaims any responsibility for the accuracy or adequacy of any positions taken by you in your tax returns. Thank you for being part of our community, and we're excited to continue guiding you on your crypto journey!

Learn how exchange fees can lower your crypto tax bill in the USA this year 2024.

Are you ready to File your Crypto taxes? Then make sure you do it right. Learn what crypto tax forms you'll need and how to report your crypto activities to the IRS before April 15th.

Earning income through crypto mining? This guide will help you understand how your mining rewards are taxed in the USA.

.svg.png)